I want to do a mini-series on three big US tech stocks to see if these can qualify as value investments. The three I will be looking at are Google, Facebook and Microsoft. Alphabet is thus the most mature of the new era Tech stocks, Microsoft represents the old guard and Facebook is the most significant new pretender to the crown.

Google is best known as an internet search engine and the company also has various other assets including YouTube, maps and email. Google is so well known it has its own entry in the Oxford English Dictionary. So pretty much everyone in the West uses Google and knows what Google is.

Google makes money by selling advertising. The principal activity historically is advertising placed within the search engine. Google has spent years making its search engine the best search engine. Define 'best'? Well it is all about relevance. Google has created algorithms that deliver highly relevant search responses to queries made by users. It can even anticipate your query based on your previous searches and likely popular searches. Having created a very user friendly and relevant search engine they then monetize this by placing adverts within the search engine results.

Relevant adverts.

Essentially businesses pay Google money to appear at the top of a relevant search. For instance type Sofa into Google and note the [Ad] responses;

|

| Google Search: Sofa |

Now this is very subtle and very powerful advertising. I showed this to my parents. They had no idea the first results were adverts. And most people don't go as far as page 2 of the search results. These adverts are also highly relevant - I want a sofa - here are the results.

Now Google is competing with traditional media such as Home Decor magazines, newspapers and TV advertising for Sofas. But this is an area businesses can't ignore, because many people buy their sofa online and these businesses need to be in the top hits to assure your custom. Furthermore the feedback from those clicks from the consumer following the advert gives you information about them and also crucially about the success of your advertising; something traditional advertising struggles to quantify.

This is why Google makes a lot of money.

Now there are a variety of other ways Google sells advertising both within its own network (such as YouTube) and through partners. Generally the shift of web browsing towards mobile devices is changing the landscape for Google. Traffic Acquisition Costs are rising as part of cost of sales as Google has to pay more to third parties to deliver its results and content. Similarly YouTube struggles to make money despite selling advertising within videos due to heavy content licensing costs. So there are challenges here and the company themselves disclose that gross margins are likely to continue to slide due to the changing market place.

It is also relevant that the 10K for Google makes several references to the cyclicality of the business. Google may appear like a utility to end users but to advertisers who bid to buy promotion costs can vary greatly based on demand. Therefore if the wider economy slows and companies pull back on promotion Google is at risk of a substantial slow down or drop in its revenues. We would expect some slow down structurally as the business matures but note the very low growth of revenue in 2009 and the strong rebound in the 2010-2012 period:

|

| Amiable Minotaur Model: Google Revenue & Growth Rate |

Therefore I think it likely that Google's revenue growth will slow down from the rapid pace of recent years both as the global economy slows and as Google reaches the peak in its share of the advertising budgets of businesses. Growing at >15% in the long term has proven impossible for any company due to the size they attain in the medium term. After disrupting the market and reaching its peak share Google can only really grow with that market and is then on the defensive against new emerging advertisers like Snap and Twitter.

Google has a brilliant 'moat.' Warren Buffet is a big fan of moats because moats mean you have excellent barriers to entry and can make above average profits for an extended period of time. Arguably the trouble with Tech is the time period is unknown and highly open to disruption; just look at how quickly the smart phone destroyed the once mighty stocks of Nokia and Blackberry.

The moat of Google is very powerful being composed of two things; (i) a network effect- because Google is so big most people 'Google' things - and the data gained makes the algorithms even better and more relevant. More people in the 'googlesphere' means more revenue and info is maintained by the company - and the more people use Google the more advertisers will want to spend there (ii) Google has intangible value that is hard to replicate - Google has a lot of patents and code that is proprietary and they spend a lot of money defending that intellectual property. That property allows them to retain their position as the preeminent search engine of the western world. They also have a lot of intangible 'real estate' like YouTube and Google Maps. These components help them further extend their advertising reach and data gathering.

How long these moats can survive is more debatable but that they exist is quite a profound reason to be interested in Google as an investment. These moats explain why Google has a fabulous 20%+ net margin.

What about competitors? Well I think Google has won the search war with Yahoo. Yahoo has really faded into the background. I cannot see the competitive advantage Yahoo has. It is smaller than Google in a market where size matters and it doesn't seem to offer any differentiation or have many useful associated family companies to rival YouTube or Google Maps. Yahoo is a bit like AMD vs Intel - this is a winner takes all market.

Have a look at this graph of market share in the UK:

|

| https://www.statista.com/statistics/280269/market-share-held-by-search-engines-in-the-united-kingdom/ |

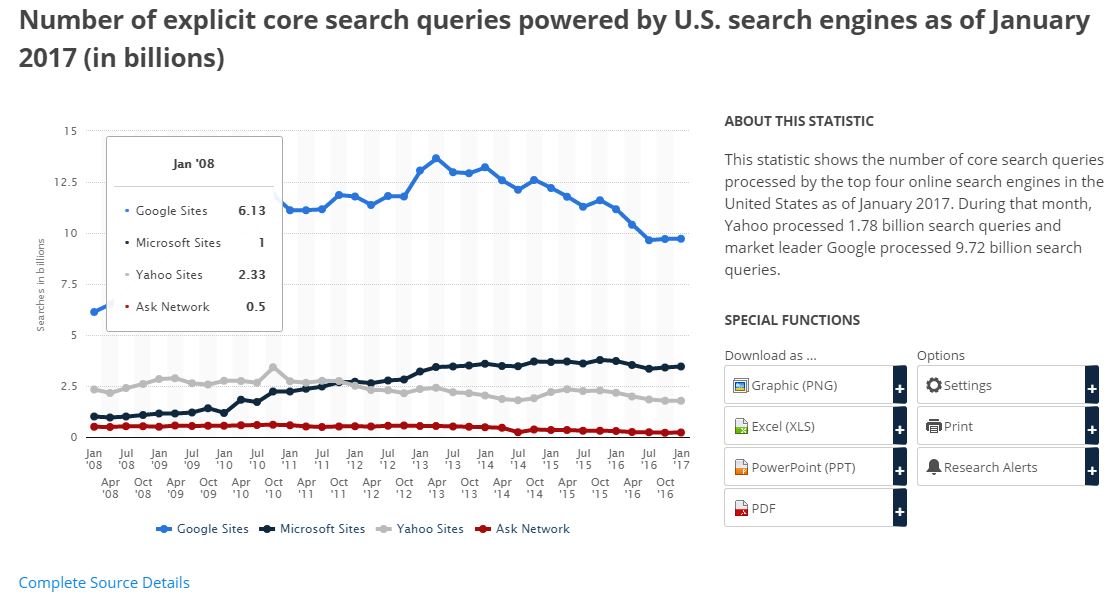

Or this from the US:

|

| https://www.statista.com/statistics/265796/us-search-engines-ranked-by-number-of-core-searches/ |

This indicates as well that the real emerging competitor is none other than Microsoft with their 'Bing' platform. Still a lot of catching up to do but this could damage the future growth rate of Google.

International competitors like Baidu and Yandex do have more of an edge as they are more effective in their home markets of China and Russia than Google has managed to be. Google is therefore probably resigned to be the search engine of the West principally the US, Europe and the Americas. So Google is marginally more a play on developed market advertising growth and economic cycles than emerging markets.

Still globally Google is king, especially in mobile;

You will find more statistics at Statista

You will find more statistics at Statista

The shareholder structure at Google means that the founders retain 56.8% of the voting control even though the bulk of the economic capital of the business is held by outsiders. This is because the class B shares held by the founders have 10 votes per share, the class A shares have one vote (NYSE:GOOGL) and the class C shares have no votes (NYSE:GOOG). The A voting shares trade at around a 2% premium to the nonvoting. The way I see it if the founders will always retain the B shares you may as well have the cheaper nonvoting C shares because your A share votes aren't worth much. It is not a terrible structure for shareholders but generally non-flat structures do not ring well with me. This means management can go about overspending on pet projects in Alphabet when I want maximum shareholder return from Google - and there is nothing I can do about it.

Google does not pay a dividend. Google has $86.3bn in cash! (2016; $118 net cash a share) Google say they have no plans to pay dividends in the future but short of a major acquisition it is difficult to see what else they can do with this huge cash pile. I think this is like the early days of Microsoft - you always have high internal rates of return and want to retain all your cash for new opportunities and acquisitions. But Microsoft has been paying dividends now since the time Google was listed (2004). I suspect in the next few years Google will too.

There is however a structural reason not to. Google has the majority of its cash offshore with $52.2bn outside the US. Should they repatriate a lot of that cash they would be subject to US taxes and this could be a significant haircut. Google currently has an effective tax rate below 20% due to substantial foreign earnings as >50% of revenues are from outside the US (Mostly Europe). However even with this in mind Google could quite easily pay a dividend in the region of 30% of profits ~$7bn a 1% yield just from annual cash generation in the US alone.

Google also has no real debt. There are $4bn worth of long term debentures in issue which seem to exist solely to build up some credit history for the company and slightly reduce the cost of capital as they have no need for the cash. If this company had a flat share structure one could take it over and take on a modest $30bn in debt and pay some serious dividends. But I don't think this will happen given the voting structure and management's aims.

Google have a buyback programme on the C shares and have been repurchasing in the last few years. The share count is still rising though due to the Tech industry preference for awarding employees with stock options. The company issued 9m shares in 2016 and bought back 5 million. The stock option expense is really quite high - although some of this could be reduced if the bull market in the shares cooled down - with $7.6bn (2015; $5.2bn) in options expenses from $19.5bn (2015; $15.8bn) in net profit. That is 39% of 2016 profit! (not adjusting for the tax effect). The paradox of stock option expense is it starts to balloon like this when your stock does well or becomes a worthless hyper inflationary certificate dole out when you stock does badly (See Twitter).

I do not think this is a good thing in the long term as a passive shareholder. Essentially Google is diluting your share value with these options and then spending a lot of cash buying back shares from the market when prices are at very high levels to compensate. This means rather than paying out that cash as a dividend to stock holders to use as they please Google are instead spending a lot of shareholder cash trying to prevent their share count growing rapidly by buying back shares in the market. If you won't pay a dividend why not just settle all the share based bonuses in cash? Unlike Twitter, Google do not need to do this in order to survive!

Which brings me to my final qualitative point; what are the incentives for management? Many of the 'other bets' of Alphabet seem to be quite tangential pet projects with limited synergies with the core search engine product. Therefore Alphabet itself is something of weird slush fund for the founders to take cash out of Google and invest it in these projects. Again as a passive shareholder I would prefer a structure that involves a more streamlined play on core Google assets - let Sergey, Larry and Eric spend their own money on developing self driving cars and smart thermostats. It is unclear whether the founders have shareholder returns as their primary focus or further innovation and side projects.

It would be nearly impossible for them to invent a greater success than Google so I struggle to see why Google shareholders should be funding these projects. Whilst at 1% of revenues the other bets are not greatly material for results the company spent $1.4bn of capex on other bets which is >10% of total capex.

It is hard to see Google reinventing itself beyond its core search product. Sure it has Maps, YouTube, Gmail etc but they all hang around this core product. Much like Microsoft with Windows and Office - they have struggled to really generate meaningful returns from side projects. I imagine Microsoft pursue things like Bing and the Windows Phone to try and keep their core products relevant.

The two great risks to Google are (a) Technological change and (b) Regulators

I think (a) is almost impossible to know in advance. Google have positioned themselves well to grow with the market and have successfully gained a greater market share in mobile than desktop searches globally. However the future is uncertain especially in tech companies so there remains a real risk of new disruptive competitors. I do not foresee those 20% net margins of today persisting into the medium term future. I.e Google has a clear competitive advantage but is it a sustainable one?

(b) Regulators are also an issue. Both from an antitrust perspective, given the near monopoly Google has gained on internet searches, and from more specific inquiries into all manner of data security, pricing, advertising filters etc. Google must have a really big legal team who work round the clock on these kind of regulatory insights. Further Google could lose valuable customers and searchers were its data to be compromised or otherwise appropriated by governments and other interested parties. Again the risks here are ultimately unknowable but very real.

A really great moat attracts irrigation projects from bureaucrats (and competitors.)

So qualitatively things I like about Google;

- It has a really big moat

- It has a preeminent competitive position

- It is highly profitable and cash generative

- It has no significant debt or pension liabilities

Some qualitative things I do not like about Google;

- The shareholder structure

- Cyclical; The business follows the consumer spending cycle

- The threat of new Tech developments

- Regulatory risks, costs and burden

- The scale of share based payments

- It doesnt pay a dividend i.e. return surplus cash

Disclaimer: I have no interest in GOOG and GOOGL shares at present. These are opinions only, not investment advice. If in doubt read my disclaimer.

No comments:

Post a Comment