Economy

The economy is primarily agricultural and underdeveloped. Nigeria has the highest agricultural output in Africa. Most agricultural produce is consumed internally by the populace.

Nigeria is seen internationally as an oil producer because oil is >90% of exports. Oil is therefore the source of foreign exchange for the country and the pole which the economy tends to swing about.

Demographics

This is a really young country which already has a massive population. The most populous nation in Africa has 187m people. In 20 years time it is projected to have 293m people. The sheer mass of humans means demand for domestic services must rise. That isn’t to say the people cant remain in abject poverty. But the huge numbers involved here and the youthfulness of the country are a profound driver for the kind of services the stock market offers – staples and banks.

|

| PopulationPyramid.net - Nigeria |

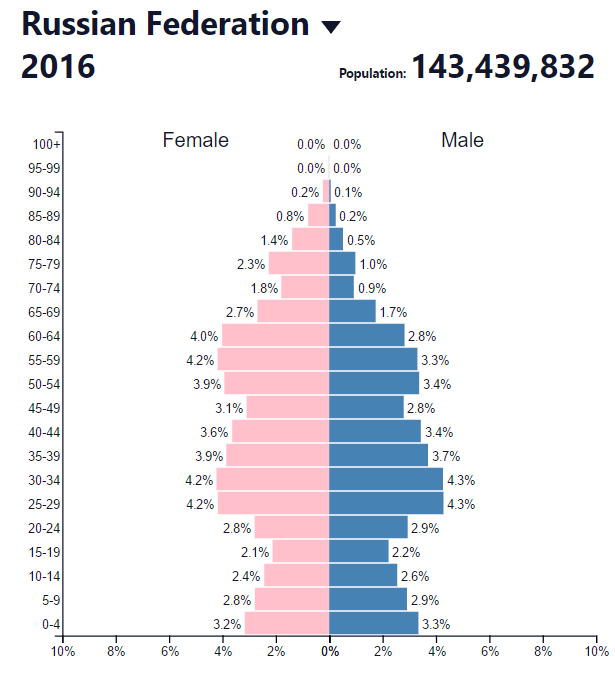

Just to make the Russian comparison again - Russia has a declining population, a resource oriented stock market (53% energy) and terrible ageing demographics where most of the men die younger:

|

| PopulationPyramid.net - Russia |

Currency

The currency should trade inline with oil prices. This is because oil exports are the principal source of foreign exchange. Dollar reserves have been falling due to the declining oil price.

|

| Trading Economics: Nigeria Foreign Reserves |

Now the currency was pegged to the dollar for a long time and recently was allowed to depreciate substantially – hence a lot of the underperformance of the market which is all Naira linked in terms of earnings (quite different from the way the FTSE 100 has rallied against the drop in GBP since Brexit).

|

| Xe.com Naira Depreciation |

Therefore the currency can’t appreciate without better terms of trade from the oil market. So again I see Nigeria as an option on higher energy prices. In the meantime the companies are doing just fine in Naira terms earning decent profits and with good cashflow. So I don’t think Nigeria is going to go bust as a nation. Note also debt to GDP is just 11%.

It is however noteworthy that there is a parallel black market rate and that the parallel rate is around the 500 Naira level suggesting a further devaluation remains a risk - but I would say a floating rate might sit between the two as often black market rates take an enlarged spread on a more realistic rate. Still a further 20-30% devaluation is quite possible in the medium term if terms of trade do not improve just given the inflation picture let alone the reserves. But this seems less of a farce at present than the Venezuelan situation.

Macro

Now they do have an inflation problem. Some of this is just par for the course in Nigeria. Inflation has been running over 8% a year since 2010. However given the recent devaluation in the Naira the rate has peaked at 19% recently. So not a great situation. But I have seen this before with Argentina – loose fiscal policy, a terms of trade shock, dwindling FX reserves, devaluation – eventually the terms of trade improve and the economy booms. For a while.

Now I am running a long-term pension portfolio here. So, I can wait. I struggle to see the market getting a lot cheaper from here but again the FX situation will likely worsen before it gets better due to the depressed oil price at present – so it could do. However note reserves have recovered slightly since the devaluation - so maybe there is light at the end of the tunnel.

Nigeria is currently experiencing a recession. The first in nearly a generation. Or at least a Nigerian generation given the rapid pace of demographic growth. But again recessions mean opportunity.

What about corruption?

Yes corruption is high, very high. But this is widely known and I think baked into the lowly valuation. I don’t imagine Russia or Argentina are any less corrupt. Now my view would change if Nigeria went fully Venezuelan but for now things look ok – they don’t have the crushing debt load nor the pure populist politics of Venezuela at this stage. But that is a highly relevant long term risk. This risk of economic meltdown would probably be most material in changing my long term investment case.

Economic 'unorthodoxy' is not per se a bad thing but when a country starts to take dictatorial decisions which act as plasters for plasters for the plasters then the downward spiral digs a very deep hole to climb out of. It is very hard to argue with the numbers and accept your fate - particularly when you are an oil nation enjoying the high life during the up cycle. Oil economies without any real industrial base really do have a poisoned chalice in this respect.

What about conflict?

This too is an issue. The Boko Haram group remain an issue for security but in general their activities have been more subdued since 2015. To be honest given how strong the market and currency were in prior years when violence has been worse I think the conflict has no real impact on the long term stock market valuation for Nigeria.

Sadly the violence continues today and it is part born of the great divisions of wealth between the rich delta Christian elites who control the oil and other groups within the populous and disparate nation.

Market Composition

Unlike the economy the Nigerian stock market is almost entirely domestic focused. As at March end 2017 39% of the MSCI index is consumer staples and 44% is banks. The residual 16% is principally cement stocks and the index has only 5% energy exposure. Now generally banks trade at lower PE ratios so this can explain some of the cheap valuation of the market. But with a Brewery and the local Nestle subsidiary making up 33% of the index the consumer staple element should be highly valued in a country with such appealing demographics.

An ETF or Individual stocks?

Global X offer an ETF which tracks the MSCI Nigeria index. The only singular stock I can buy as a GDR is Guaranty Trust Bank. This stock is 16% of the index and the biggest bank in the MSCI index. Now I would rather own the consumer staples from a pure long run demographics perspective. So the opportunity to own some GRTB via an ETF rather than just GRTB is appealing. However within my SIPP wrapper the ETF is ineligible for some reason - i think as it trades on the NYSEARCA exchange - so GRTB it is.

I do note that the banking sector accounts for the majority of the apparent cheapness of the market. Frankly the consumer stocks still trade at lofty valuations. However the banks will be the play on the upside story in the economy - so if one wants to buy an eventual recovery in the Nigerian market banks offer the most leverage to the upside.

To my mind the principal risk with the ETF is that Global X close the fund. This fund has $25m in AUM – hardly a profitable level of scale despite the relatively high fees (>1% p.a.). It would be typical for a provider to close the fund right at the bottom of the market due to the lack of popularity and scale. No other providers offer an ETF.

In summary I think Nigeria is undervalued as a stock market. I think it offers deep value investors a long term option on a country with exciting demographics and cyclical upside improvements to its terms of trade.

Having studied Argentina in depth in my time and seen the massive rally in Argentine banks and utilities generally following the fall of the Kirschners I can see the potential huge upside of nations which appear at present to be ‘garbage’ for sensible investors.

Things I think make Nigeria a Value play:

• A very cheap stock market by global standards trading on 6x-9x PE

• Domestically focused stocks

• Currently the country is in the midst of a cyclical downturn in terms of trade and currency

• Highly favourable demographic trends for consumer focused growth

• It is off the radar and generally disliked - $25m in ETF assets globally!

Things I think make Nigeria a Value trap:

• Corruption is rife and conflict risk is high

• Cyclical improvements are out of the control of the nation and make take years

• The country may become increasingly populist and dysfunctional (the Venezuela model)

In Part II I will have a look at GRTB for bottom up red flags to the apparent cheap valuation.

Disclaimer: I have an interest in GRTB as mentioned in this article at present. These are opinions only, not investment advice. If in doubt read my disclaimer.

No comments:

Post a Comment